More resources for advisers

Our Challenger Adviser Knowledge Hub has a large range of resources for advisers including product and technical information, articles and guides.

Movements in the price of oil have a significant effect on the economy. An increase in the oil price both adds to inflation and suppresses economic activity, two effects that could be particularly damaging in the current economic environment.

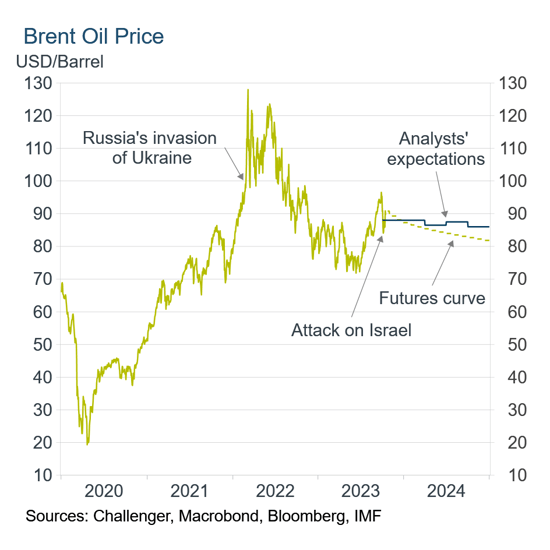

The price of oil has been on a wild ride over the past few years. Expected demand slumped with the onset of the pandemic in early 2020, with the price of Brent oil slumping to $20/barrel (all prices are in US dollars). The price rebounded strongly alongside the economic recovery.

The oil price spiked with Russia’s invasion of Ukraine but as supply adjusted and demand eased given tighter monetary policy, the price fell back.

Oil supply and demand

While shocks to actual or expected supply, such as from Russia’s invasion of Ukraine, have an important impact on the oil price, as the past few years have highlighted, movements in demand can be a bigger driver of the oil price. In recent years China has accounted for much of the global growth in demand for oil.

The slowdown in economic activity globally over the next 1–2 years from tighter monetary policy (and higher inflation) will ease demand for oil and put downward pressure on the oil price.

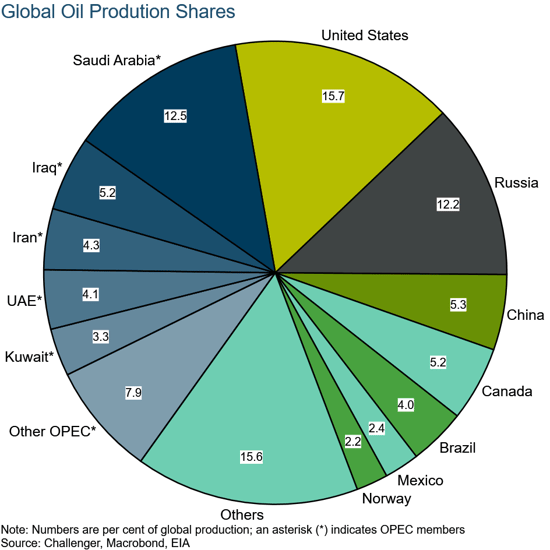

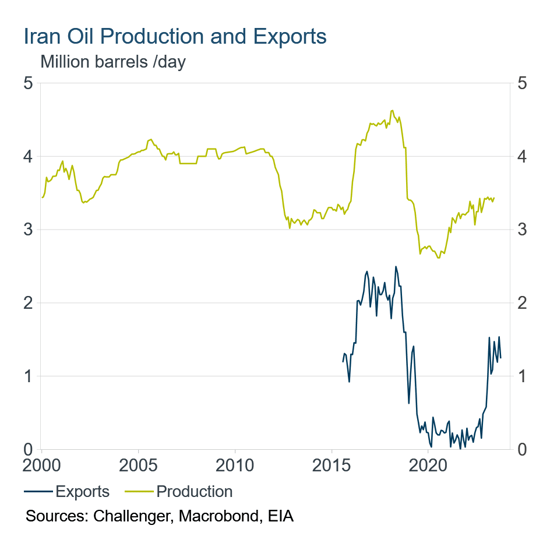

But currently there is a greater focus on the impact of events in the Middle East on the oil price from the potential impact on supply. While the oil price spiked by over $20/barrel when Russia invaded Ukraine, the jump was much smaller for the attack on Israel. Russia accounts for 12% of global oil production and significant sanctions were imposed on its oil exports, but Israel and the very immediately surrounding regions are not significant producers. The $4/barrel jump following the attack on Israel reflected a small risk premium for the chance that existing sanctions on Iran could be tightened if it was implicated in the attack. While sanctions were imposed on Iran, which accounts for 4% of global oil production, when the agreement on its nuclear program broke down these sanctions have been loosely applied recently enabling Iran’s exports to recover to around 1.5 million barrels/day having been close to zero for several years. The risks from a broader escalation in the Middle East are significant given tankers travelling through the strait of Hormuz transport about 17 million barrels/day of crude oil and refined products from Saudi Arabia, Iraq, Kuwait and the United Arab Emirates.

The price impact from the potential for a tightening of sanctions on Iran has been moderated by the view that there is spare oil production capacity in other countries that could make up for Iranian oil. Saudi Arabia is estimated to have spare capacity of around 3 million barrels/day, and the United Arab Emirates and Iraq over 1 million each. Whether Saudi Arabia or other countries would increase production in response to a tightening of sanctions on Iran is uncertain given geopolitical rivalries and the greater assertiveness of OPEC+ countries in adhering to output caps.

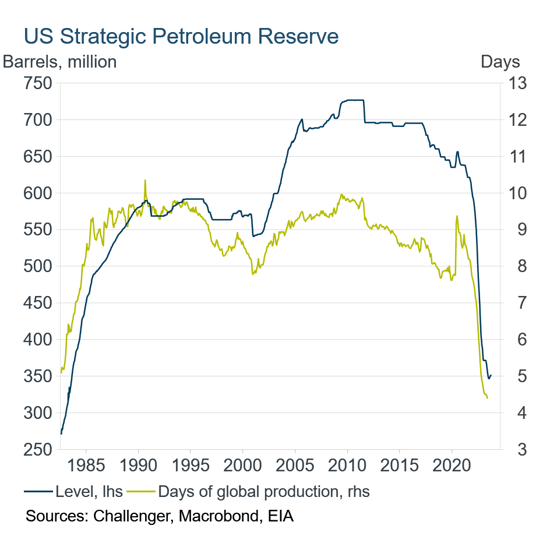

Another dynamic to the net supply of oil comes from the United States’ Strategic Petroleum Reserve (SPR). The SPR was established in response to the 1970s oil embargo to protect the United States given at the time it was a net importer of oil (it is now a net exporter). The size of SPR holdings was reduced gradually from 2017 to 2021 in response to high oil prices. Large withdrawals were authorised by the President from March 2022 following the invasion of Ukraine and resulting jump in prices. Once the oil price had fallen back below $80/barrel in late 2022, SPR withdrawals ended.

While the SPR is currently only half of its full capacity, the United States could release some oil in response to a jump in the oil price from an escalation of the Hamas-Israel war.

Where to from here for oil?

While there is a risk that the oil price could jump higher if there is an escalation in the Middle East, most analysts think this is unlikely. Private analysts’ expectations and those of the US Energy Information Administration suggest the price will remain around $90/barrel. This is consistent with the relatively small jump in the price of oil when Israel was attacked (since oil can be stored, a high expected future price will lead to an increased current price) and the futures curve pricing a gradual decline over the next 1–2 years. Overall, given flexibility of supply and the belief that the Israel-Hamas war will not spread in the region, a sharp rise in oil prices is not expected which is good news for inflation and economic activity.

Related content

How bad are recessions for asset returns?

Is inflation higher for some households?